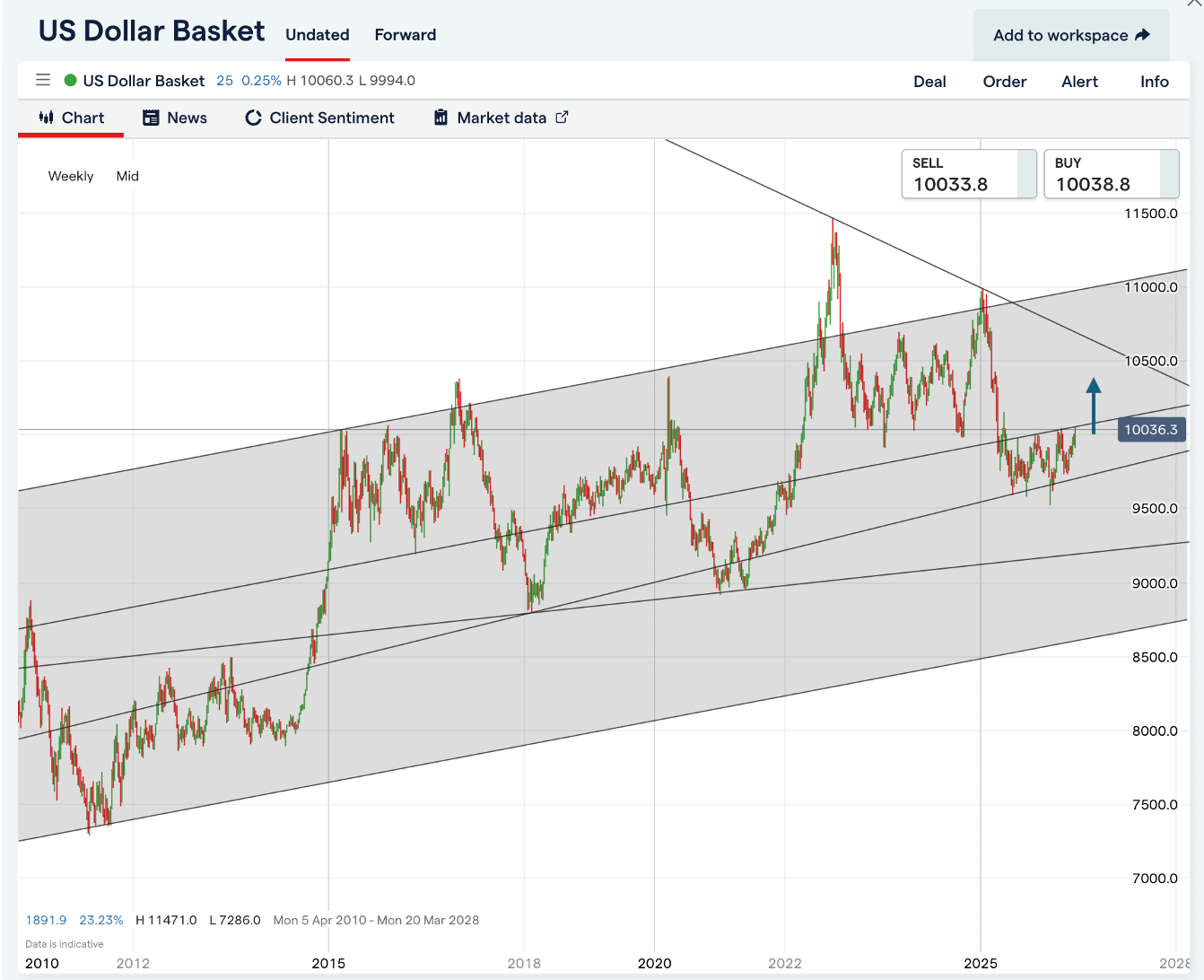

Dollar breaking higher to new range

Losing its risk premium, a good week for the US, Trump gets his victory lap

The break higher

The dollar is finally making a run at the top of the range. Breaking decisively above 101 on DXY is the view I outlined in the 5 June Dollar Watchtower. Why? The main catalyst expected was a hawkish swing to hard money under Warsh, and a general shift by G10 central banks in risk management approach to inflation. While not completely shock & awe, the combination of ECB & BoJ rate hikes, with a hawkish-enough tone from Warsh delivered the thematic tailwind expected.

The USD stands to gain the most from a perceived shift in central bank inflation mentality, as the dollar has had a heavy risk premium holding it back through a period of substantial US growth and risk asset out-performance. Trump policy volatility, a poorly constructed dollar debasement thesis, continued reliance on fiscal stimulus, albeit, in much more productive forms, tariffs . . . all these factors combined into a risk premium - ball & chain around the dollar’s neck.

Positive news on both monetary policy and fiscal policy in 2026, no matter how small, will work to lift this risk premium and allow the dollar to break out of its range. The US growth & earnings story can finally be fully validated.

A move up into the 101-105 range would be sufficient recognition of the improvement in dollar fundamentals. Which probably equates to a EURUSD move down to 110-12 and sterling move down to 1.28-30. The wild card is USDJPY. Without intervention, the Yen is unlikely to strengthen, and yet, deep undervaluation and better Japan economic performance makes USDJPY-higher a poor risk/reward trade.

The capital flow case for Yen is that it is the most liquid high beta proxy on US ex-AI growth. Limited market cap leads KOSPI and TAIEX to become quickly overvalued when global capital pivots at this point in the cycle, while the Nikkei has plenty of room to absorb more. And JGBs, while not exactly flashing red-hot buy, are now high-yielders vs China, Taiwan, Singapore and Thailand. Japanese corporate bond yields are also becoming globally competitive, with investment grade bonds like Rakuten’s recent issue yielding 4.7% (about 50bps below the US, but 50 above Europe).