Solid US structural inflows, but dollar weakness

Strong 2025 inflows, equity vol rising, dollar still correcting

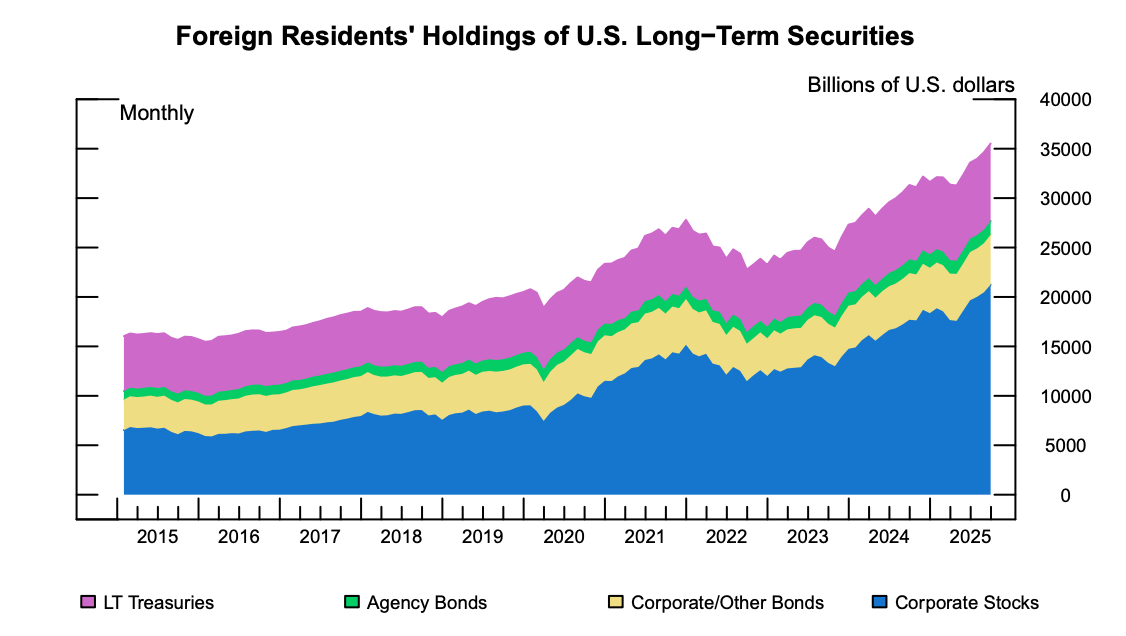

US inflows

With so many negative stories and shocks in 2025, it may seem surprising that USD hasn’t really changed in the past 8 months. DXY is basically unchanged from April last year. As the full year 2025 cross-border flow data start to print, it is easy to see why. The US saw over $300bln FDI inflow, up 10% from 2024. Likewise, TIC data recorded a $1.2trl inflow into US long term securities, a nearly 50% increase over 2024. The private sector is clearly showing no US market avoidance.

Most of the negative headlines and angst derive from diplomatic tensions, creating fear that official flows will change course. The truth is, COFER data have been pretty stable since 2020. China is allowing its FX reserve/treasury portfolio to roll off at maturity, Japan is reinvesting maturities, and UK/Europe custody holdings rose. This is a story of FX reserve saturation as a hedge, not a strategic shift from dollar utility as liquidity backstop. Basically, most of the world doesn’t need further FX reserves to perform its liquidity buffer function. They’re all portfolio investors now.