The dollar's complex breakout to the upside

AI Deflation, Stellar earnings, Trump domestic focus, US-China strategic stability

The range break

I’ve written a number of pieces this year on the DXY Index range and what scenarios might be needed to break the range (14 Apr, 26 Mar, 3 Feb). From the first report in Feb I divided 2026 into anfirst half/second half story, as the calendar begins to add constraints from next month.

Trump started 2026 prioritising geopolitical gains. The script argued for a Q2 wind down so that June-Oct was all about celebrating the World Cup, 250 year anniversary, and victory lap on growth. This would give GOP the best chances to win at the midterm election. There was a moment in early April when the market called this neat timeline into question. However, now, as we conclude May with a ceasefire holding and a successful US-China summit concluded (strategic stability as a détente framework for G2), the scenario and timeline have gained traction.

What does that mean? The DXY Index range top-side breakout for the second half is now the primary trade. First quarter GDP was solid, and corporate earnings shot the lights out. My Feb stylised factor weights were:

60% - Growth & Risk Asset perf

15% - US-centric factors

10% - World Order shifts

5% - Valuation

5% - Intervention & forced sellers

3% - Interest Diffs

2% - National security imperatives

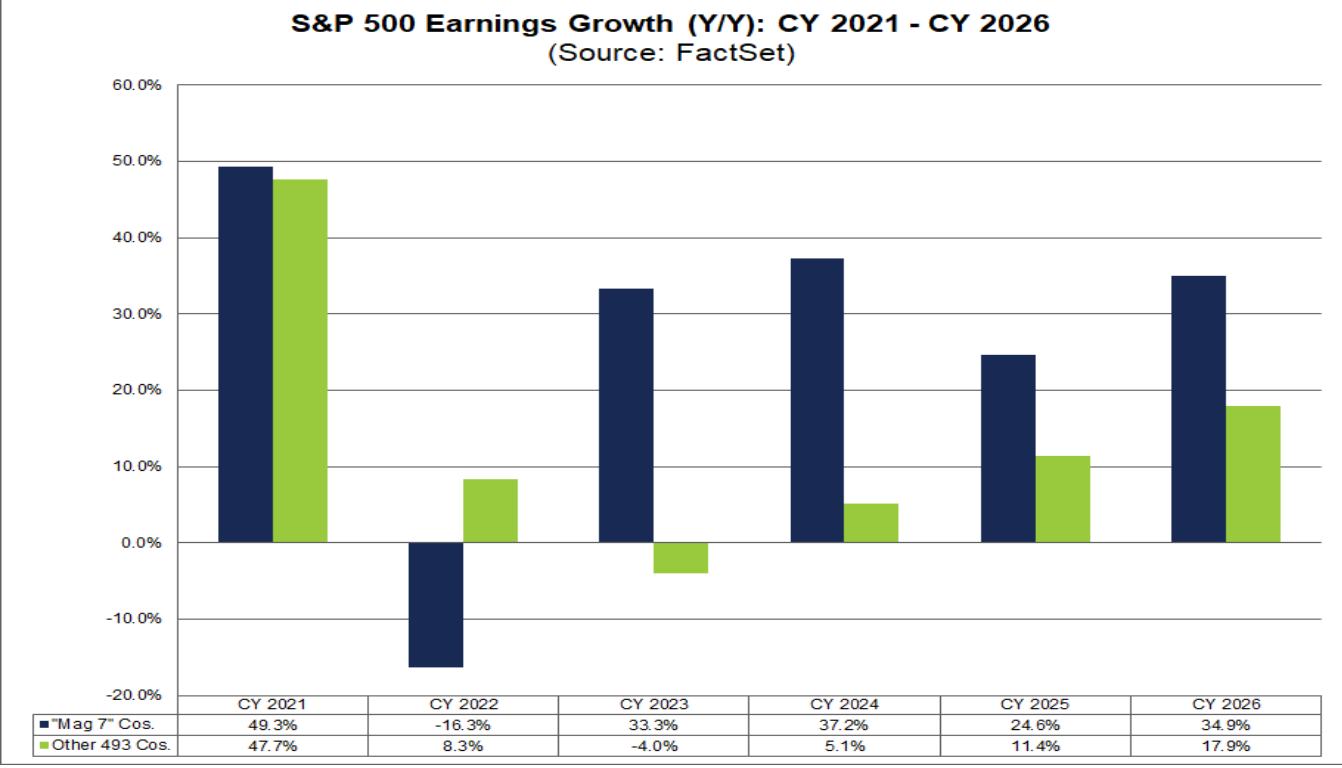

The US earnings story powered through the uncertainty and strongly rewarded all those overweight foreign investors. That’s how you sustain high valuation.

84% of the S&P companies have reported EPS above estimates, which is above the 5-year average (78%). This was not only a Mag-7 story. Mag-7 exceeded estimates by 32.5%, but the rest of S&P exceeded estimates by 16.6%. The broad market earning story is building and gaining moment.

And the outlook remains bullish. Estimated earnings growth for 2026 for both the Mag-7 (34.9% vs. 24.3%) and the other 493 S&P 500 companies (17.9% vs. 14.7%) are higher today compared to March 31, as analysts have increased full-year EPS estimates for both groups.