USD-HKD carry trade can be an early sign of USD consolidation VS Asia

Following the surge in Asian currencies during April, and then the sharp drop in USDTWD, HKD traded to its upper band, triggering intervention from the HKMA.

(https://www.hkma.gov.hk/eng/news-and-media/insight/2025/05/20250520/)

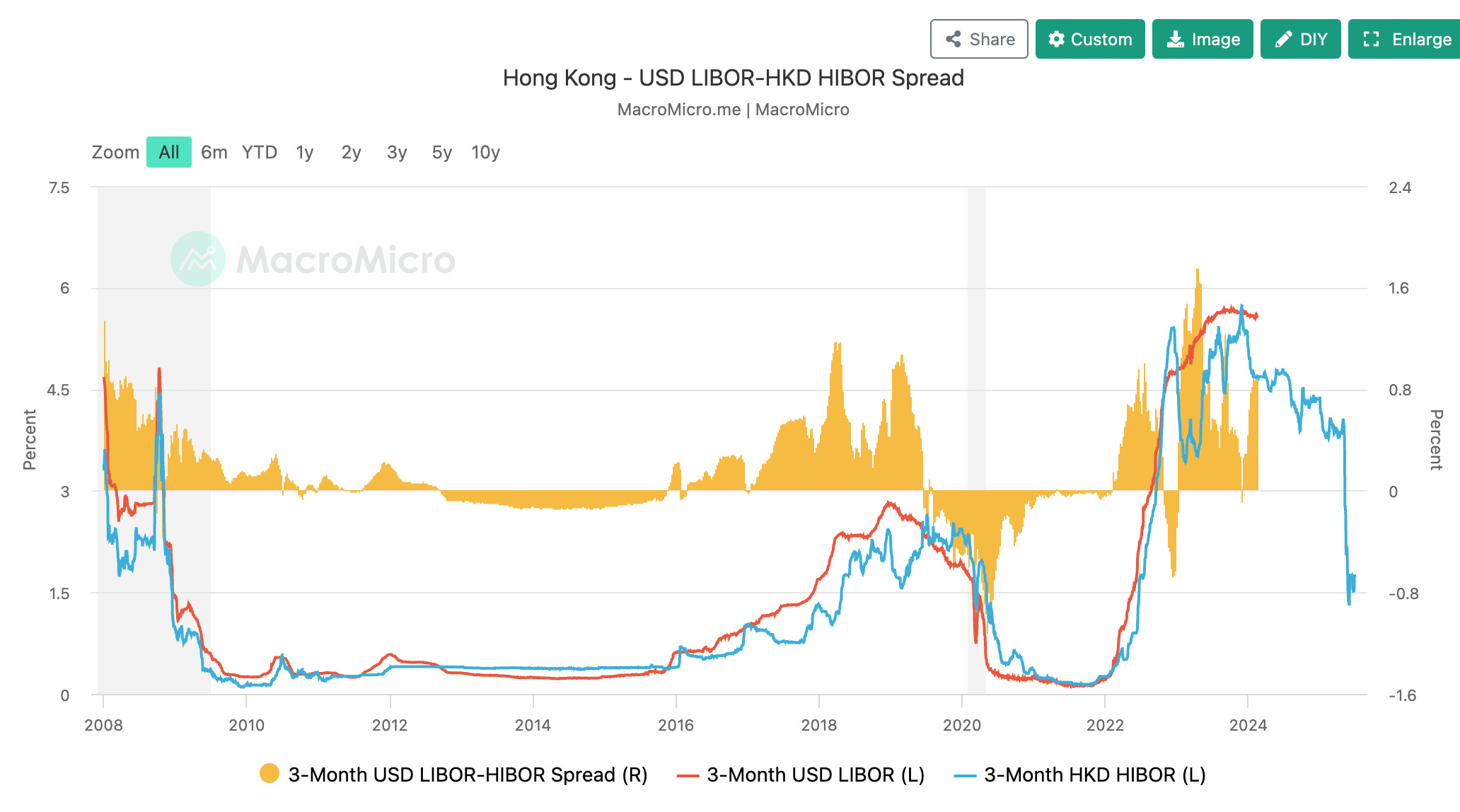

Liquidity injections then pushed HIBOR to its lowest level since 2022, pre-inflation shock.

HIBOR rates have continued to sit at low levels as the excess interbank liquidity slowly dissipates, but the traditional arb trades, or USD-HKD carry trades, are not forth coming. While FX vol (cited in the Nikkei article link) is certainly a reason to fear going long some USD-ASIA carry trades, HKD shouldn’t be one of them. The HKMA will be managing liquidity in your favour.

Therefore, new flows into the USD-HKD trade might be an early normalisation signal that USD-ASIA will consolidate as well. Pressure on USD-TWD appears to be building again, so perhaps fresh news on Taiwan lifer’s USD hedge ratios is needed to take the fear out of the market. I think we can expect COC to handle the lifer’s USD hedge flows differently this time, as well. Some smoothing should be tolerated without sending red flags to Trump’s Treasury office. The story has been well communicated by this point.

It is true that late June was more about pricing higher odds for early Fed rate cuts, but given how far financial conditions have eased since Apr/May, the Fed is going to need some hard data indicating a growth slowdown before they take any risk on tariff-impacted inflation outcomes for this year. In the interim, the dollar’s consolidation VS Asian currencies will be driven by changing views on Trump policy stability. Long USDHKD makes for a cheap, early entry for that trade.

https://asia.nikkei.com/Business/Markets/Hong-Kong-interest-rates-fall-despite-currency-s-US-dollar-peg